There seems to be a lot of rumors, suggestions, and ideas floating around about secondaries but little hard data … so Tod Sacerdoti, Jeff Lu, and I decided to survey 100 founders (93 responded) of some of the largest tech companies about secondary transactions: and here are the answers.

Our hope from this survey was to help inform what the current best practices are.

On a personal note: I’ve never done a founder secondary transaction myself and likely never will (though one of cofounders at LiveRamp did a secondary). But if I did do a quality secondary transaction at LiveRamp, we likely would have never sold the company and instead took it to IPO (and thus have had a significantly higher return for our shareholders). So secondaries could add a lot of value – especially for founders without a significant previous exit.

As an investor, I have been an investor in many start-ups that have done secondaries. Meaning some of the old shareholders sold some or all of their stock. I have also participated in buying secondary shares of companies on many occasions.

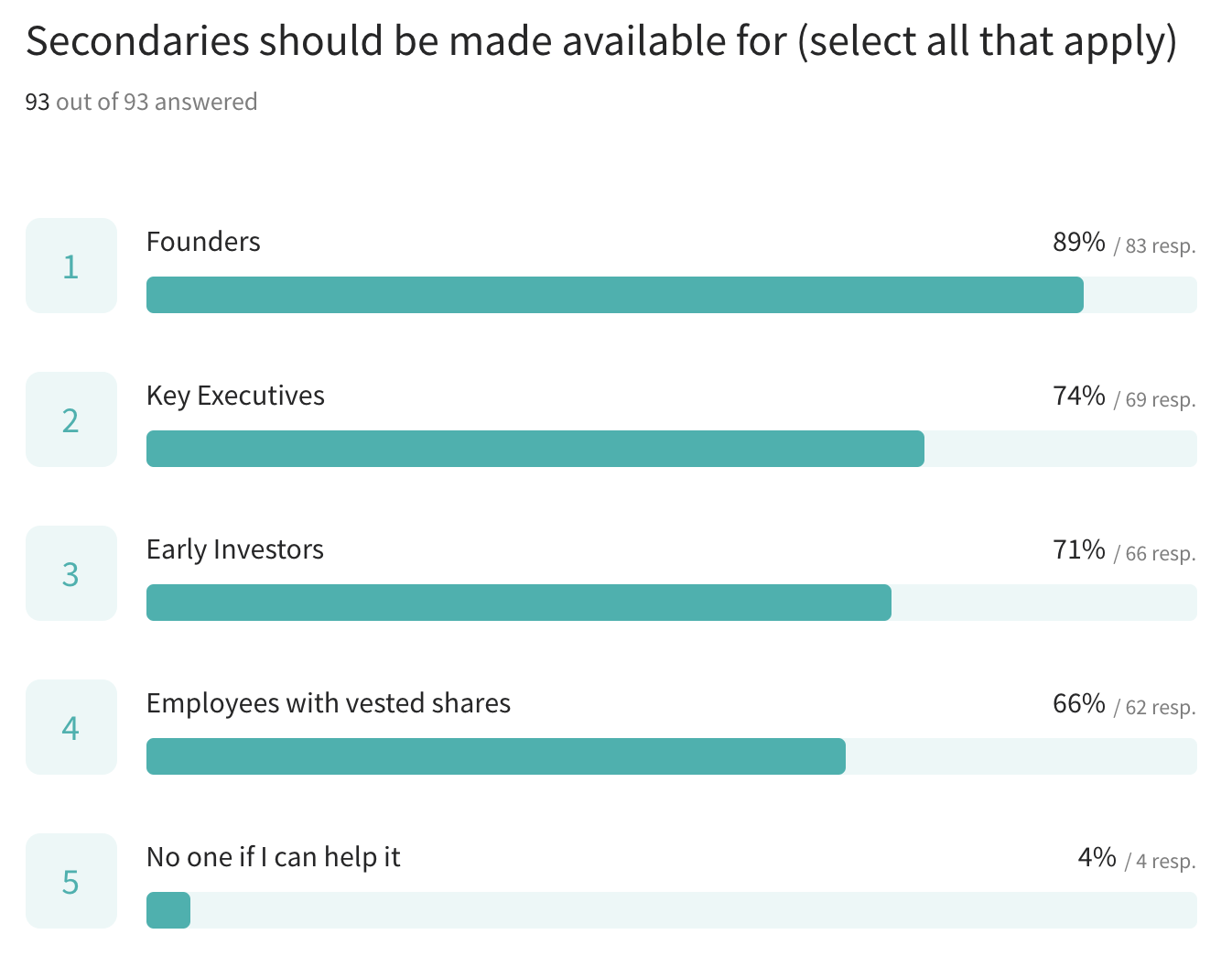

In the first question, we got some requests for a sixth option for “early employees.” We didn’t want to change the survey in the middle to skew results, but we did want to flag that as some feedback. For the most part, it seems like everyone is open to secondary for a broad swath of stakeholders.

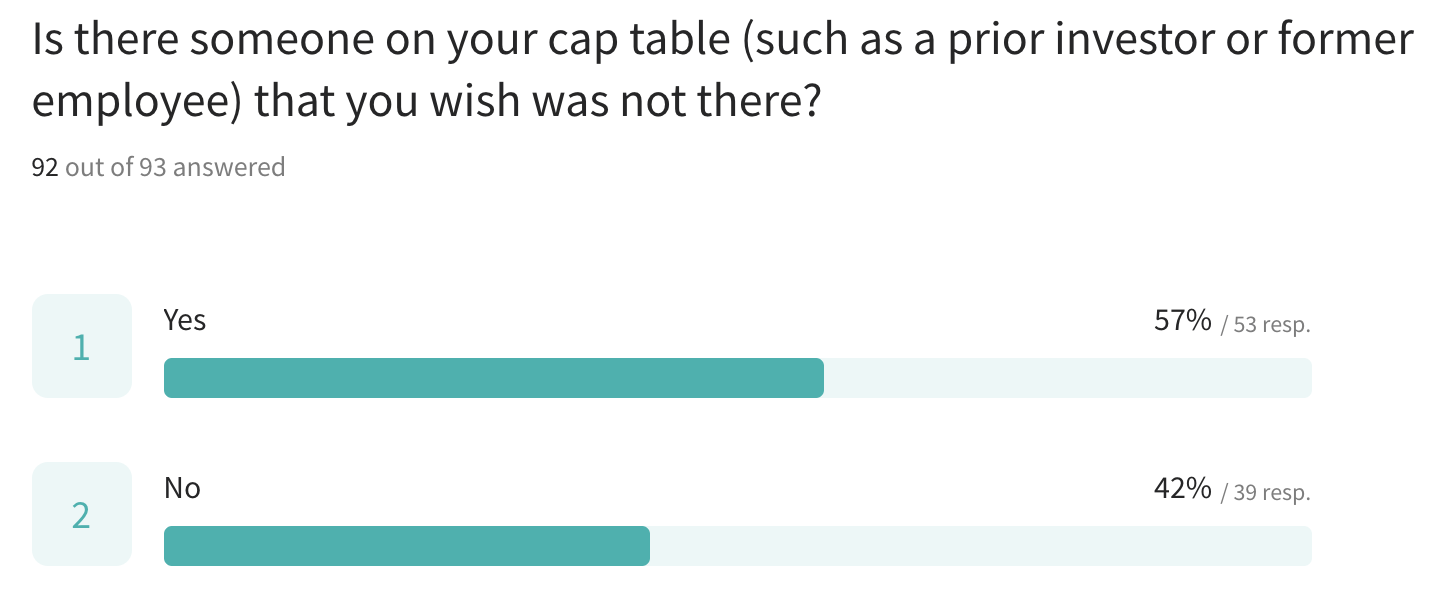

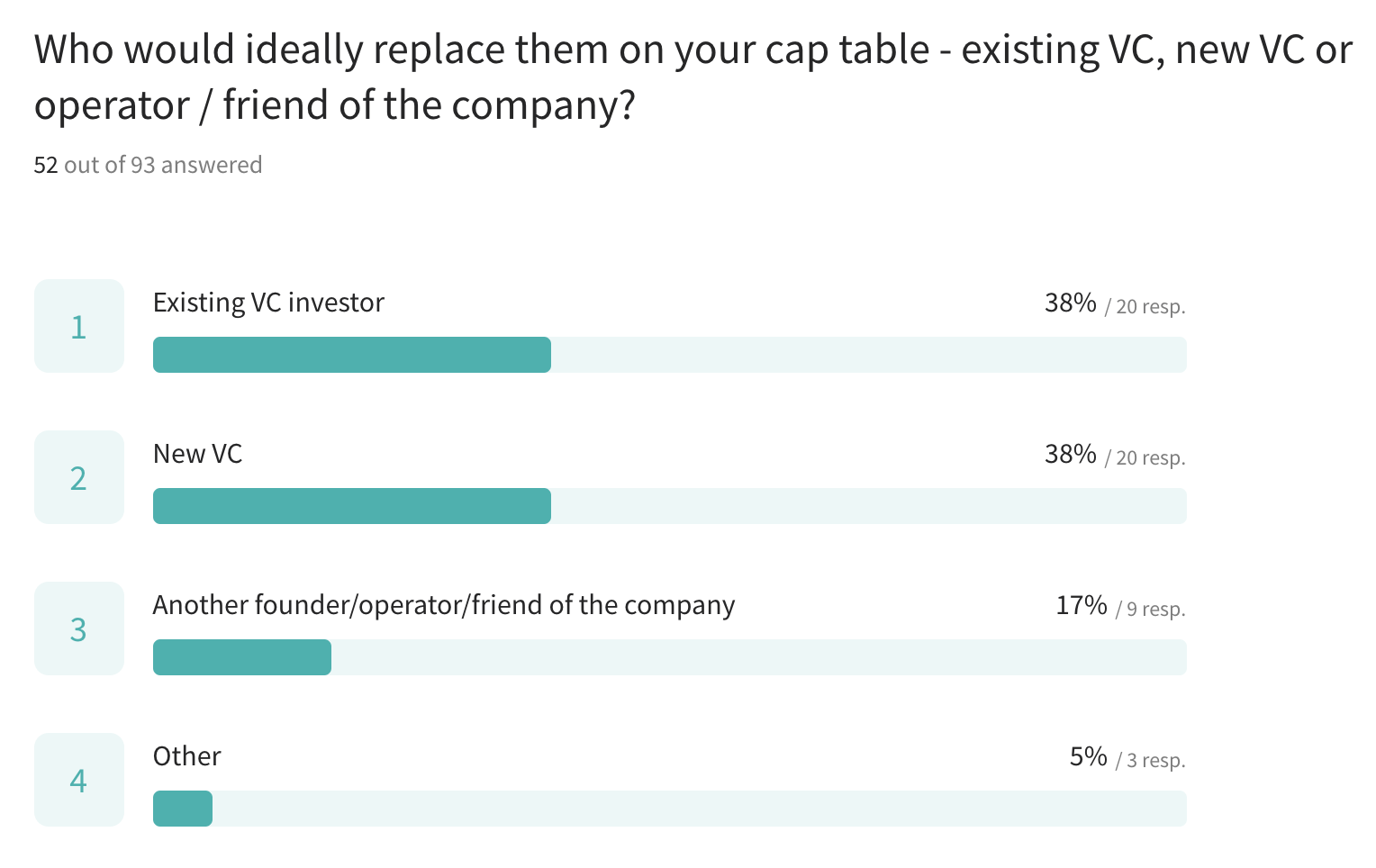

The next 2 questions go together. A little over half of the respondents have someone on their cap table who they regret having. Interestingly, in those cases, over 50%+ would prefer a new investor or operator/friend to buy the troublesome investors out vs. their existing investors.

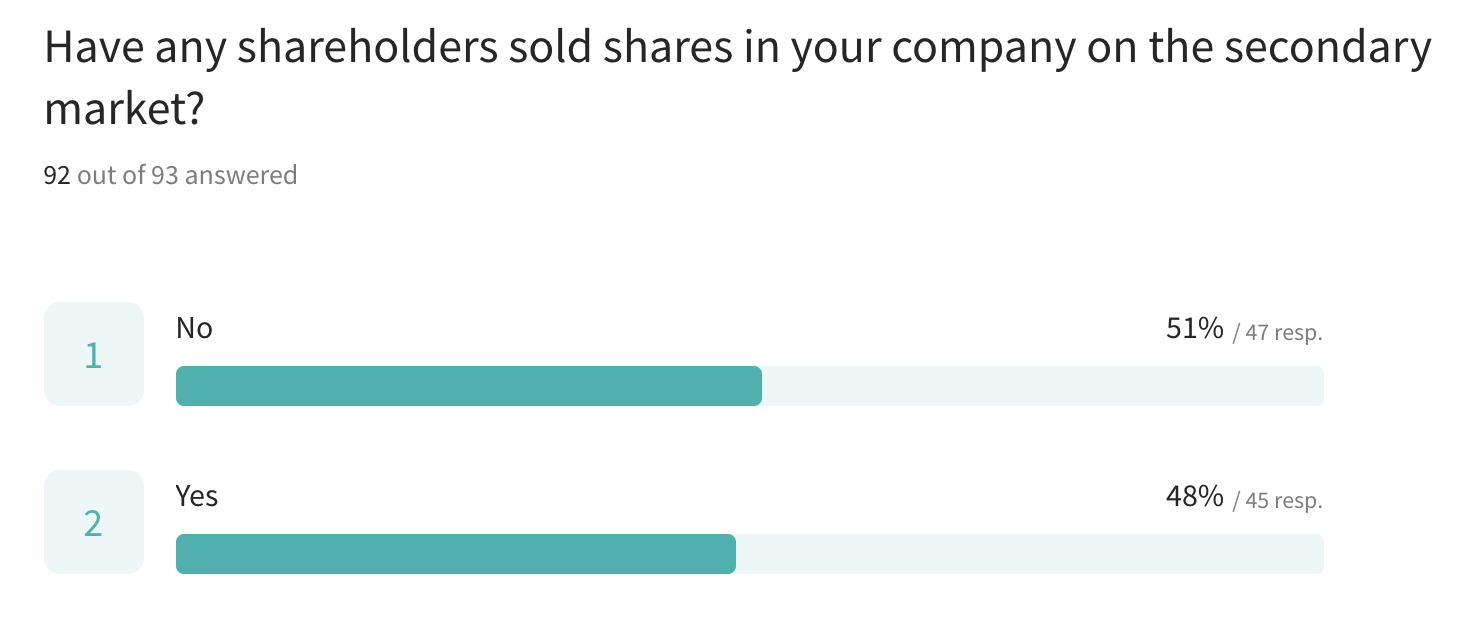

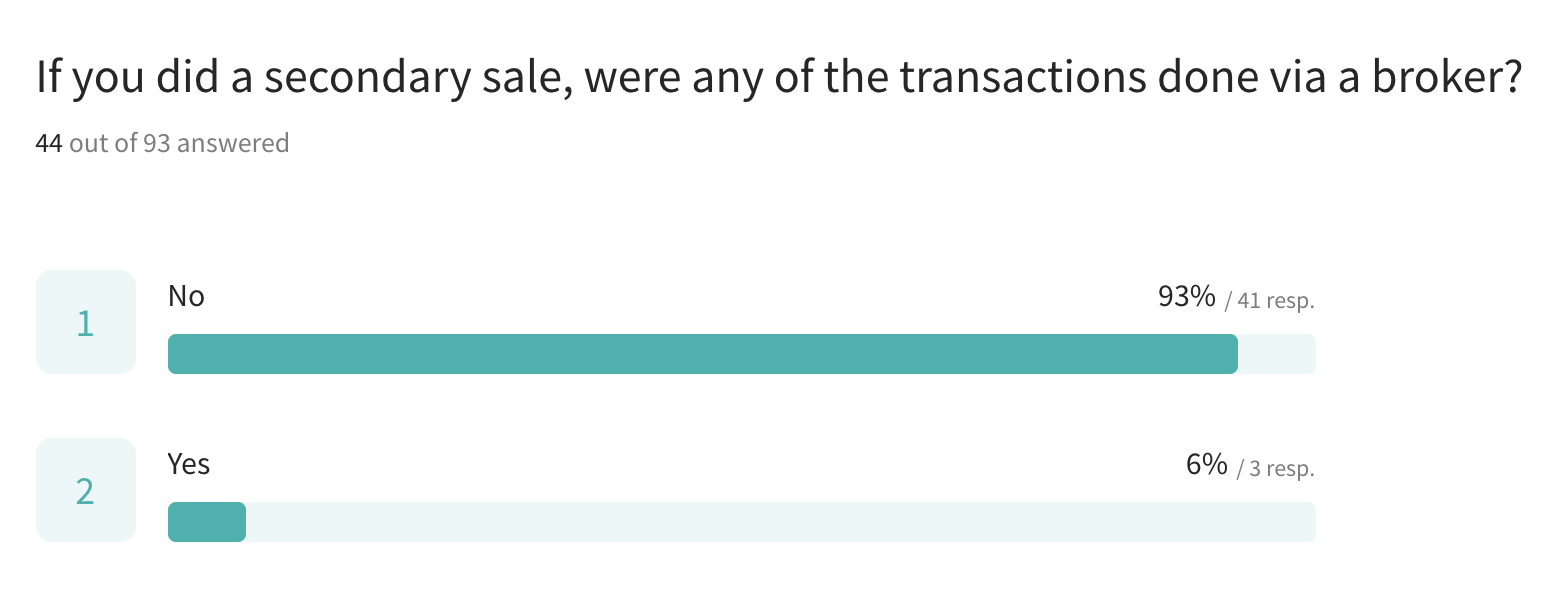

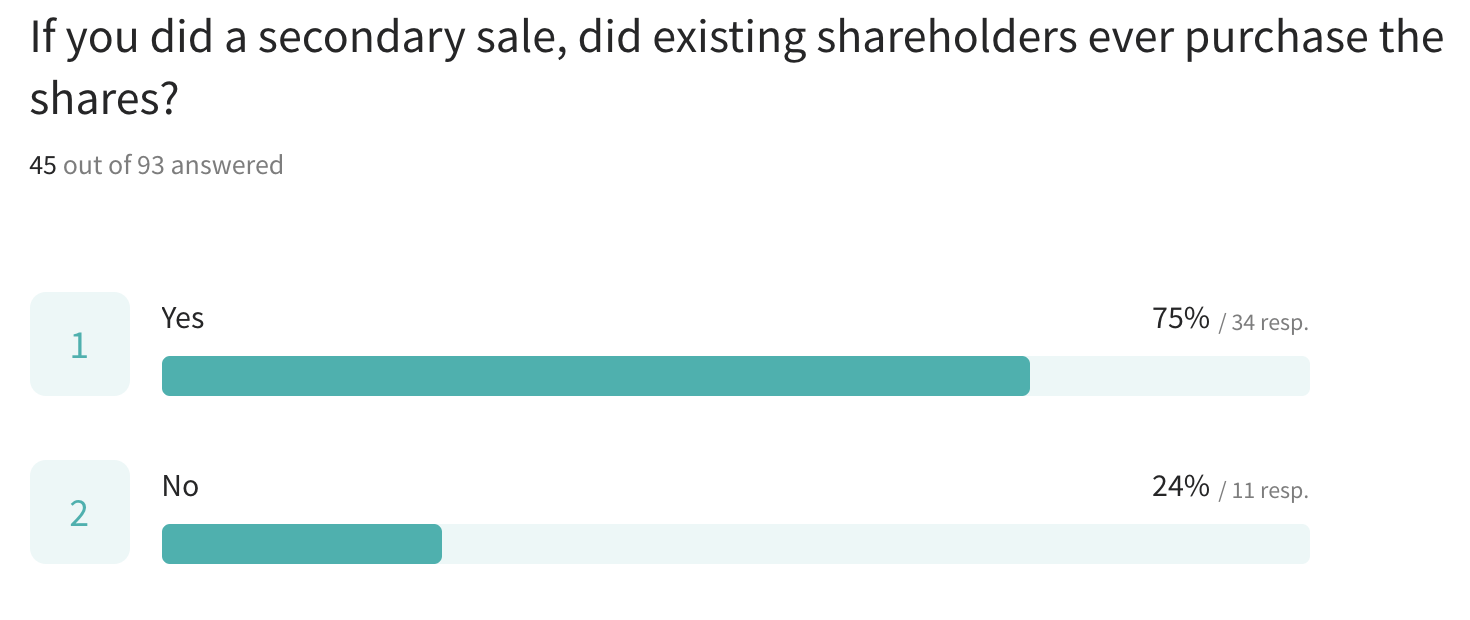

Half of the respondents have experienced secondary sales at their companies. Very few were executed via a broker (6%) and 75% of the buyers in those transactions were existing shareholders.

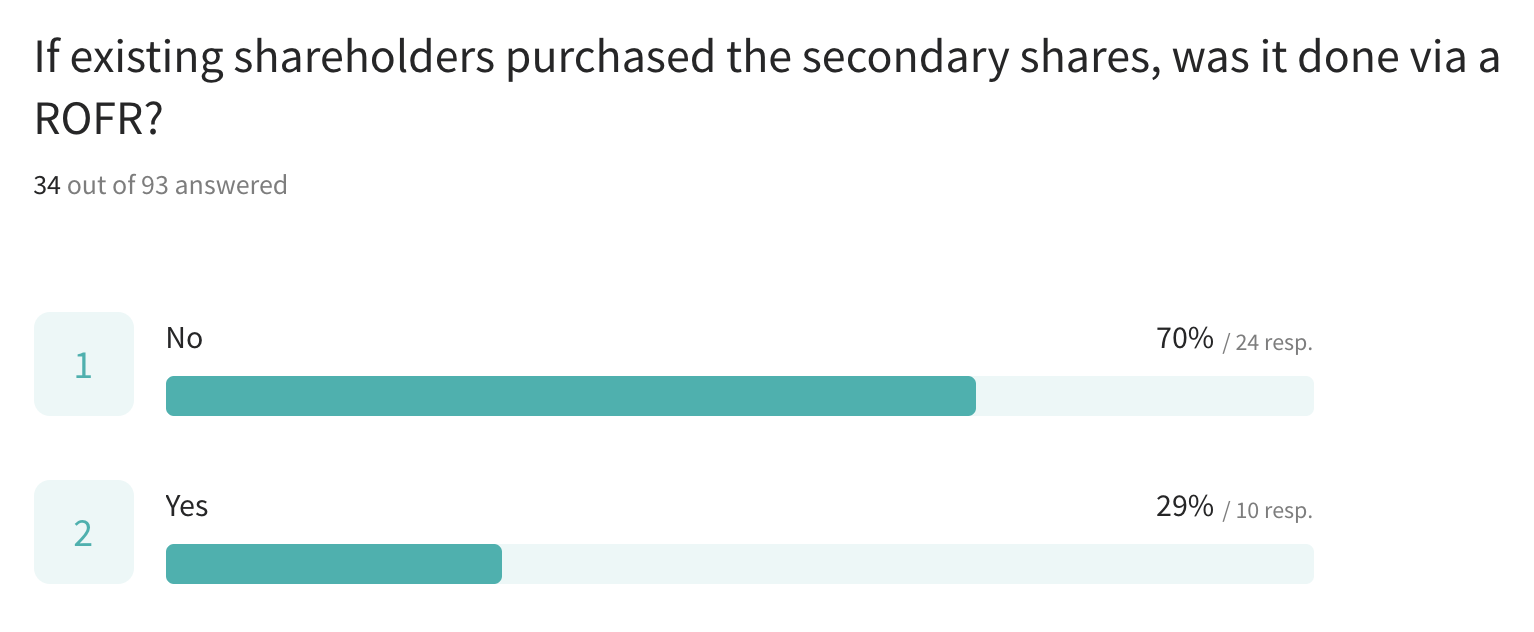

Despite the fact so many transactions involve an existing shareholder as a buyer, only 29% involved the insider executing their ROFR. One explanation is that most of these secondary transactions may be catalyzed by an existing investor, rather than initiated by an outside offer.

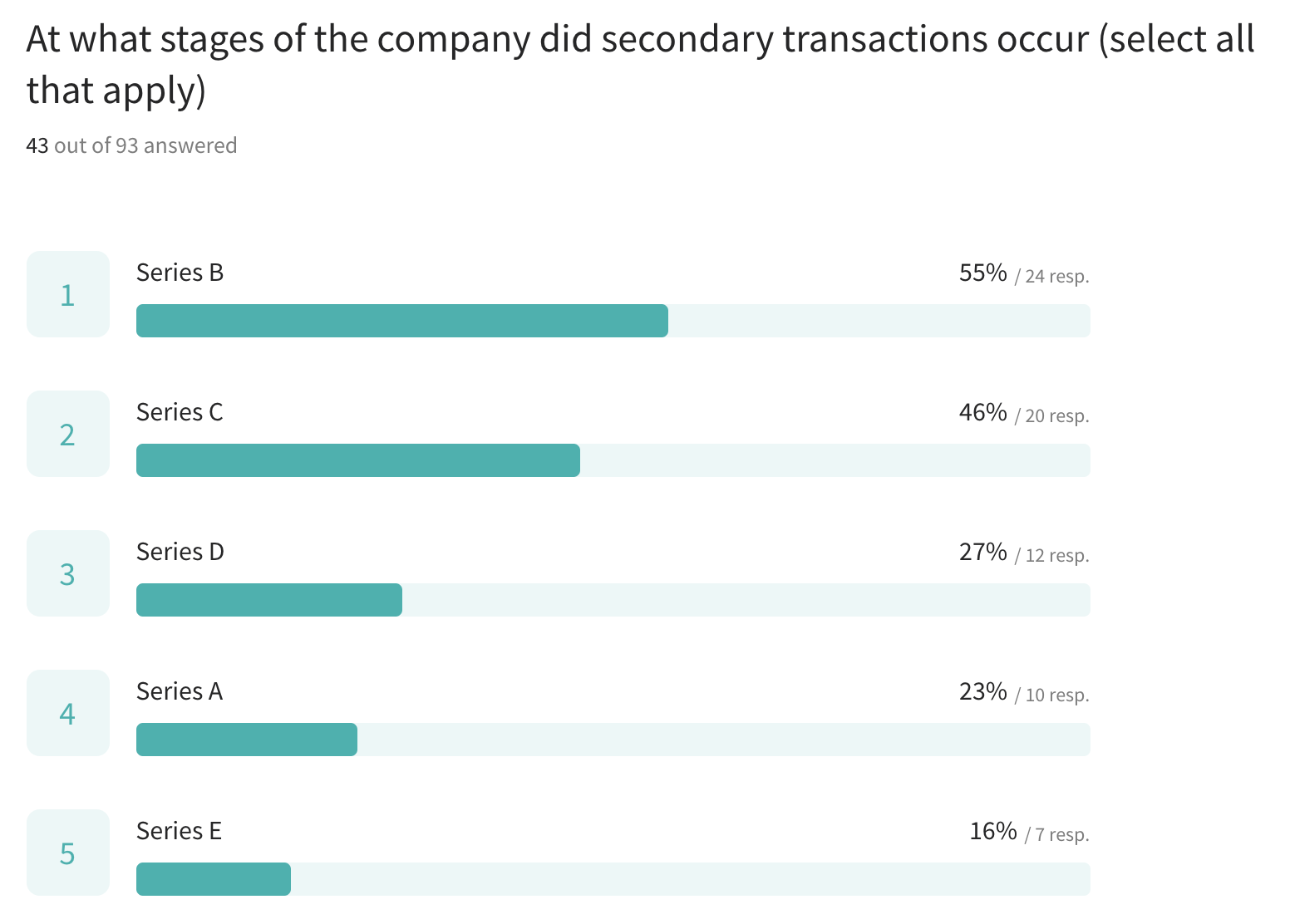

Secondary sales are happening at all stages, but Series B-D is the most popular.

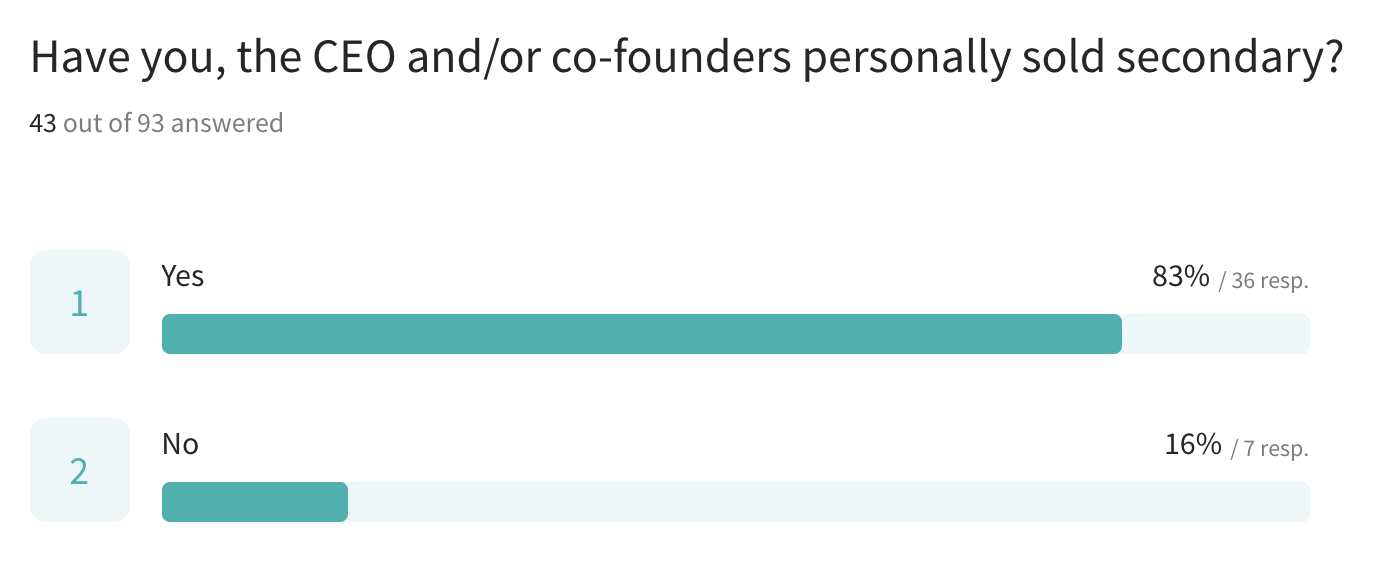

Of the 45 CEOs who have had secondary sales occur at their companies, 80%+ have personally sold shares. This also makes sense as a large number of companies in our survey are unicorns with a lots of liquidity options.

Note: Tod, Jeff, and I have done a few other founder surveys and will be publishing some of findings in the next few months. Ping me if you are a founder and want to participate in these anonymous surveys.

Thank you for doing this! Covering the kind of stuff where there is not already a lot written out there is super helpful. I have been an active angel over the last couple of years, and have come to view my role as an angel to be to help the Founders with the money/advice/connections they need to get them to an institutional round. I invest at first check/f+f/pre-seed and would love to sell to one of the first institutional vc rounds that come in (A or B, etc.) that is a high enough IRR for me, takes risk off the table and gives me more money to invest. I’d love to get some advice on the right way to approach this – so it does not look like a negative signal, overly complicate the Founder’s life, etc. Do you recommend approaching the Founder? At what point? In instances where angels sell their shares to the VCs coming in, do they get the deal price (assuming they have pref shares)? Thanks very much in advance.