Warren Buffet once famously stated that compound interest is the eighth wonder of the world. Power laws rule much around us, but more so in the technology and business worlds. One fantastic deal, such as Facebook buying Instagram, can shift the bedrock of business everywhere. Despite the common belief that 80% of company acquisitions are failures, the remaining 20% can shape a new path for in that company – the expected value is still enormous and is definitely a worthwhile path if executed properly.

M&A is generally a net positive even though most acquisitions fail.

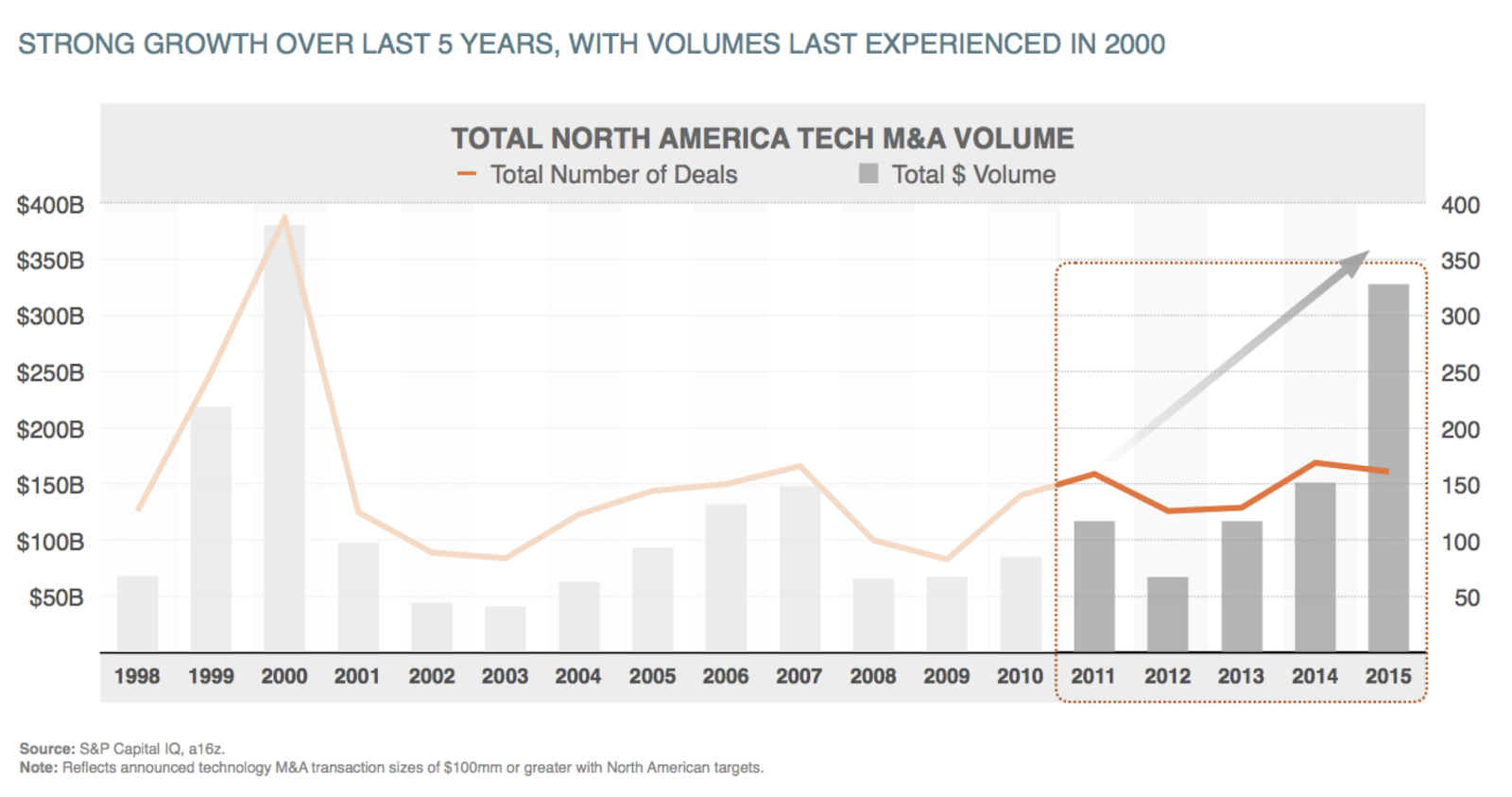

80% of company acquisitions do not work, but when they do work, they can work spectacularly.

Acquisitions, like tech investments, follow a power law.

Many people mistake averages for value. Venture capital is exactly the opposite of this: missing the seed round of AirBNB if you had the chance to invest means you would be financially worse off than had you invested in 50 Theranoses. The difference is that in the first case you would make 1000x your investment or at worst 0, so the opportunity cost is immense.

Power Laws also exist in company acquisitions.

The Power Law of Company Acquisitions is why companies continue to make acquisitions. In the few cases it does work, like Google’s purchase of YouTube, the gains can continue to reap dividends decades later. Fundamentally, most of the best acquisitions are contrarian in nature; otherwise, they would have been bought by another company already. And sometimes, like the YouTube acquisition, there are only a few companies that could have acquired it successfully – the key is to stay within your circle of competence.

M&A strategy is under-rated. Great M&A can transform the company.

In some cases (@bookingcom, @LiveRamp, @VMware, etc.) the acquired company became more valuable than the rest of the parent.

Summary: in this post you will learn when to take the time to use first principles and the three rules for thinking.

There are tons of people that claim you need to use first principles for all things. People I follow and greatly respect (Naval Ravikant, Shane Parrish, Julia Galef, Eric Weinstein, Scott Alexander, Peter Thiel, Elon Musk, etc.) regular promote first-principle thinking.

The problem is that you cannot use first principles to determine everything. You don’t have the time to do that. You need to rely on proxies who you believed have figured things out and believe in them (until you eventually figure out that the proxies are wrong, frauds, etc.).

For instance, I have never actually done the full proof that the world is round. I don’t actually know, with 100% certainty, the shape of the earth. I use proxies to help me determine that. It might not be round. There might be a conspiracy. Or we might be living inside a simulation. I’m not 100% sure. But I rely on proxies and make an assumption that the world is round (at least for my purposes).

I don’t know (with certainty) that the moon landing in 1969 was real. Some people believe it was faked. But I use proxies who I respect and therefore adopt the belief that the moon landing was real. I believe this even though I have not taken the 100+ hours to prove it myself.

Therefore, I believe the world is round and also believe the moon landing was real. Am I 100% certain? No. But I live life believing it and know that I will likely never take the time to prove either to myself.

Let’s say you are investing money in something, what is the rate you want to be scammed?

You could, of course, say that rate should be zero. That you will tolerate no loss due to scams, unethical practices, etc. But that puts an extreme due diligence burden on you before you make an investment. You can’t be 100% on BOTH precision and recall. If you have fewer false positives, you will inevitably have fewer false negatives.

Being skeptical of everything will allow you to avoid investing with Madoff, but it will also have you miss that angel investment in Facebook and Airbnb. Many ideas seem very crazy (until they aren’t).

This is also true in life.

You can distrust every taxi driver and every construction contractor … but that might lead do you distrusting most people which could lead to a lot of unhappiness.

Or … or … or … you can accept that you will have some rate that you will be scammed.

You should have a rate you want to be scammed.

A good rate is likely 1-3% of your interactions. This can be on taxi cab drivers, investments, hires, etc. If your scam rate is under 1%, you are likely not taking enough chances. If your scam rate starts approaching 10%, you might lose all your money.

If you never get into a car, you will never die in an auto accident. But you will also have a lot of trouble living life. So you need to have some guide-rails (wear a seat belt, don’t get in a car with a drunk (or sleepy) driver, etc.). The same is true for investing or doing anything else in life.

Rapid raise in stock prices result in some people in the company being overpaid. This can be very bad for the overpaid employee and also very bad for the company.

Many tech companies are going public right now and many tech companies have seen significant share price increases in recent years. We can expect that most of these are facing real internal motivational challenges that could be extremely hard to overcome. The weirdness of RSUs in public companies

Let’s say that a company gives you an offer of $100k salary and $500k in RSUs vested over 5 years. That essentially means that the company values you at $200k per year (as stock and salary are fairly fungible in public companies).

Let’s say the stock goes up by 20% after six months. The RSU grant (over 5 years) is $600k and your yearly comp goes from $200k to $220k (a 10% increase). No big deal for the company as you are probably worth more than 10% more than what they originally offered you because you now have been at the company for 6 months, understand the processes there, have grown your skills, etc.

But now let’s look what happens when they stock goes up by 300% after 3 years (which happens in the tech world). Now the original grant of $500k is now $2 million (over 5 years). So the stock alone is $400k per year. Add in the salary (with assuming some raises is now $150k/year) and you pulling in $550k per year.

This is when things get a bit hairy. Because likely the company only values you at $350k so you are making $200k more than you are worth. In fact, if you quit the company and went to work for its top competitor, you might have a hard time getting more $300k.

When you are evaluating a business (to invest in or join), one simple heuristic is to understand how easy is it for the business to get new customers.

In B2B businesses, the metric that companies track is CAC (Customer Acquisition Cost). But this metric in itself isn’t that interesting and companies typically track LTV/CAC ratio where LTV is the LifeTime Value of customers. The problem with this ratio is that many companies are constantly focusing on the numerator rather than on the denominator.

The cost of acquiring the next marginal customer should be less than the cost of acquiring the last customer. And you should see this cost decline over time.

The CAC itself should decline each month. If it does, it means you likely have a great business. If it doesn’t, the business is a good business at best.

Of course, CACs should be declining for a specific cohort of customer. If your business was only focused on small businesses and now you are selling to enterprises, your CAC will increase dramatically. In this case, the key thing is to track the CACs for SMBs and enterprise customers separately (with is why so many firms use the LTV/CAC ration to simplify this step).

The best way CACs will decrease over time is if you haver some sort of network effect. LiveRamp (my last company) is a middleware company … which means it is essentially a marketplace of buyers and integration partners. It is a classic network effect business that makes it easier and easier to acquire new customers over time. Once we hit about $10 million, the CACs started dropping fast.

One other way to think about this when selling to enterprise is to track the quota for a full ramped sales rep. Is the quota for an average sales rep going up over time? If so, you have a great business. If not, the business still has some work to get to great.

Simplest heuristic to tell if a business is great (rather than just good): is the cost of acquiring customers declining https://t.co/bWRyIdpSwE

All platforms follow this logic. Companies like Plaid, Segment, Marqeta, LiveRamp, and Carta are classic platforms where acquiring new customers gets cheaper over time (disclaimer: I’m either an investor or friends with the CEOs of all these companies). These types of companies can take the savings (from not having to invest as much in sales and marketing) and put them into the product. So the product can get better and better over time (which is the double-edge flywheel that all great companies have).

Other companies that have declining CACs are ones with great brands. Essentially every time a company buys their service (and raves about it), other companies are more likely to use it. Twilio and Stripe have declining CACs because they have become the default go-to companies in their space. There is a LOT of power in being the default.

Summation: Once a business gets over $10M ARR and it has declining CACs, it has the makings of a great business.

Old lessons die hard.Everyone of a certain age has heard the VHS verses betamax tale.

VHS was an inferior technology to betamax but it won out due to marketing, etc. After hearing enough of these tales, one starts to wonder how important a better product actually is. Is it all about marketing? That was the moral of the VHS story.

Turns out a better product … even a slightly better product … is REALLY important.

One interesting case study is Zoom — the videoconferencing solution. Now let me put my cards out there: I use Zoom at least once a day. SafeGraph uses Zoom (and Zoom rooms). I like Zoom and would recommend Zoom. And we pay for Zoom (it isn’t free).

Why does one pay for Zoom?

Well, you might say that you need a videoconferencing solution, you evaluated the market, and choose Zoom. Maybe Zoom is more expensive than its competitors but it is the best so it is worth paying for.

The problem with that logic is that one of Zoom’s most feature-filled competitors is Google Hangouts. And Google Hangouts is “free” if you are already a Google Apps customer (which 99% of technology start-ups are).

So there is a choice to be made. Google Hangouts which is a very good product and is effectively free. or Zoom which is a better product (but not massively better) and is also pretty expensive.

Tons of companies need to make this choice. A lot of them have chosen to go with Zoom (as evidenced that Zoom is one of the fastest growing B2B companies). Why is this?

Of course, from a customer’s perspective, free is much preferred than paid. My company chose to use Google Drive rather than Box or Dropbox because we thought Google Drive was pretty good and did not think Dropbox or Box was enough of an improvement to justify their very high enterprise cost.

So for video conferencing, why don’t people choose Google Hangouts over Zoom?

First off, to state the obvious, Zoom is actually better than Google Hangouts on almost every dimension (the one dimension that Hangouts is superior is that it has a better integration with Google apps: no surprise there).

So if you are choosing to go with Google Hangouts verses Skype or verses GoToMeeting or verses Webex or verses one of the other dozen video conferencing systems, choosing Hangouts (because it is free and it is very good) is a no-brainer decision.

But Zoom is just better enough that people are happy to pay for it. Well, they might not bee “happy to pay” exactly. No one loves spending money. But companies are certainly willing to pay for Zoom. Zoom Rooms is an amazing product and they have really focused on a great user experience. The Zoom video quality is really strong. The mobile experience isn’t wonderful but seems to work better than most of the competition.

One of the things that Zoom proves is that you can be extremely successful even when you have a crowded category, lots of great competition, and when even your strongest competitor is giving away the service for free.

Twenty years ago no one would think that a company like Zoom would thrive.

One of the biggest trends that is driving Zoom’s success is that companies are forgoing the full stack and buying the best-of-breed. The number of vendors the average company is buying from has increased almost 10x in the last 12 years. Companies are happy to buy from many different places … they are even happy to buy from new start-ups.

In fact, it has never been easier to sell to large companies. Large companies are open for business. They want to be sold to. They are sick of having a third-rate solution. They want to use the best product. If you can show them your product is superior, they are excited to buy.

The best product is actually starting to win. Sales and marketing and partnerships are really important (as is brand), but it is so much easier to market a great product than one that is fifth-best. Even amazing companies like Google, Microsoft, Oracle, SAP, Salesforce, etc. are struggling to get their clients to use products or features if they are deemed sub-par by the customer (even when they bundle it in for “free”).

That wasn’t true 20 years ago. In the 1990s, it was really hard to sell software to a big company for less than $3 million. You had to hire Anderson Consulting (now Accenture) to integrate the software. So big companies spent most of their money buying from a very small number of big trusted vendors. And they mostly had a fourth-best solution across their stack.

Today it is much easier to buy. The SaaS revolution has changed everything. Big companies can dip their toe in the water and start for $10,000 per yer in many cases. So even if it doesn’t work out, no one gets fired. It is a low cost option to try out the later and greatest technology.

Even the most crowded markets and even those markets dominated by amazing companies are open to new ideas, new products, and new companies.

Having the right vendors is as crucial to one’s success as having the right employees … and in the case of large companies potentially even more crucial (because it might be impossible for a large boring company to hire the best people in the world but it is still possible to get the best vendors … because a software vendor will sell to everyone).

In fact, one of the best ways to evaluate a company is looking at what vendors it has. You should have a really good idea about the sophistication of the talent, the ability to move quickly, and how fast the company can respond just by knowing which vendors it uses.

Before I invest in a large public company I personally like to review what vendors it employs (you can get the data for free on a site like Siftery). The list of vendors is essentially like a DNA snapshot — no two companies are alike … and like DNA, there are some genes that are just better than others and some genes that work with each other better.

Summation: we need to take new learnings from the old lesson that superior products lose to superior marketing. While both are important, the quality of the product ultimately trumps the quality of the marketing.

Enough better than hangouts that they are doing really well.

Data companies fall in four quadrants: Truth verses Religion and Data verses Application

If you are thinking of starting a data company, you have to make a very important choice: what kind of company will you be? There are four basic types of data companies and all can be very successful … but the biggest mistake data companies make is that they try to do more than one at a time.

First let’s define the x and y axis…

Truth verses Religion

Truth companies are backward looking. They tell you what happened or when something happened or something about a person, product, or thing. The main objective of these companies is to have true data. Good examples of truth companies are a credit bureau (like Experian, Equifax, and Transunion), middleware (like LiveRamp, Segment, Improvado, and mParticle), and financial services data (like large parts of Bloomberg). These companies are usually very long on data engineers.

Religion companies predict the future. They tell you what will happen based on a set of data. The main objective of these companies is to accurately predict the future. Good examples of religion companies are credit scores (like FICO), fraud prevention (like ThreatMetrix), and measurement (like Nielsen, Market Track). These companies are usually long data scientists (and sometimes machine learning engineers).

Religion companies often purchase data from truth companies. For instance, FICO uses the data from the credit agencies as the core ingredient for its credit score.

Data verses Application

Once you have a valuable set of proprietary data, you have to choose if you will be a pure data company or if you will build an application on top of your data.

Data companies just sell data. The best way to know if you are a data company is if you have no UI or a very limited UI. Data companies sometimes sell direct to end buyers but often also sell to applications (which is why it is so important they do not become applications as you do not want to compete with your customers). Good examples of data companies are in financial services (like Yodlee, Vantiv), a pure data co-op (like Clearbit), location (like SafeGraph), wealth predictions (like Windfall Data), and others.

Applications make data sing. To really get benefit out of data, you need an application. These companies will have nice UI and more front-end engineers. Good examples are query-layers (like SecondMeasure), refined datas co-op (like Verisk and Abacus), integration layers (like Vantiv, Plaid), B2B product usage (like G2Crowd) and others.

Winners and lowers and winner-take-most markets

For a “truth” company to dominate its field, it has to be clearly better than everyone else. And “better” means its data needs to be the most true AND the market needs to believe it is the most true. In addition to truth, breadth and price are very important to dominate.

For “religion” companies, the most important factor is brand. When predicting the future, ideally you want to believe that the Nostradamus within the religion company is making accurate predictions. And while some people may dive into the Bayesian logic, most will trust the market perception. That’s why there are so many poor predictive analytics companies, because one can buy brand with money.

Series beats parallel

The biggest mistake data companies make is that they attack more than one quadrant at once. For the first $100 million in revenue, you should be focused on just one type of business.

Summation: Older people (over 50) are getting more advantages from computers than younger ones. We should expect to see a huge renaissance the productivity of older business people in the future.

In business, there are advantages of being younger and advantages at being older. And historically there has been tensions between the two.

Many advantages of Being Younger

Fearlessness: Youngers people have less fear of older ones. They have less to lose, less social status, no mortgage. If they fail, they will not be lower on the status ring. The best soldiers are usually those in their 20s.

Older people have much more to lose and that means they are often quite poor at calculating risks.

More time: The older you are, the more time commitments you gather. You eventually get married and have kids. You volunteer at a non-profit. You get involved in your church. You pick up golf as a hobby. You go to the Sundance Film Festival and Burning Man every year.

When you’re younger, you have not yet accumulated the debt of these commitments. That allows you to spend more time working. Of course, not every young person spends a great deal of time working (many spend an equal amount of time socializing) … but those that do concentrate on work have a massive advantage because working hours compound. Almost all super-successful people worked insane hours in their 20s. In fact, people who do not work insane hours in their 20s are at a massive disadvantage for the rest of their lives.

More raw brainpower: Younger people have better working memory, they have more stamina, and they have more calculations per second. They have a much faster CPU. It seems unlikely that we will have a 55 year old chess champion. And most Physics Nobel prizes went to work that was done by people in their 20s or early 30s.

More ignorance of “what works”: Older people are more likely to get stuck in their ways. They have a hard time seeing that the Emperor really has no clothes. So they are more likely to do things the way they have been done before. The old saying “science advances one funeral at a time” applies to business innovation as well.

But there are also many advantages of Being Older

Money: Older people are a lot richer than younger ones. Many older people gain leverage by hiring younger people and telling them what to do. They are often able to rent the time, fearlessness, and brainpower of younger people.

Cunning: Cunning is the ability to work with people and also work against people. It is something one gets better at over time. It is not something people are just born with. A 55-year-old can often play two 25-year-olds against each other.

Wisdom: While young people benefit from ignorance, older people benefit from wisdom (which is the opposite side of the coin). Older people have had more time to read, learn, and compound knowledge.

Connections: While “What-You-Know” is now more important than “Who-You-Know”, who-you-know is still important. Older people have had more time to develop meaningful connections. And many of those connections will be other very successful people. I did not know any major CEOs, U.S. Senators, world-renowned authors, etc. when I was 22 (but many of the people I met when I was 22 turned into these people).

Stature: Older people have a history and a brand. And while that history can work against them (like a voting record for a member of Congress), it gives comfort for others to work with them. People with a brand have an advantage in recruiting talent, raising money, etc. If an entrepreneur sold their last company for $300 million, it will be a lot easier for her to recruit people to her next company than a first-time entrepreneur.

Less competition: Weirdly, older entrepreneurs have a lot less competition than younger entrepreneurs. At least in Silicon Valley, it seems there are 100 times more entrepreneurs in their 20s than entrepreneurs in their 50s. Most successful people in their 50s have no desire to go through the rigor of starting a company again. They usually opt for less stressful lives (like deciding to be a venture capitalist or running a winery). That means that those 50+ people that do decide to start companies have a pretty big advantage because there are a not a lot of wise, well-connected, monied people who they are competing with.

Young vs Old: Who Wins?

To summarize the post thus far:

Advantage

Young

Old

Fearlessness

✅

Wisdom

✅

Raw brainpower

✅

Ability to buy brainpower and time

✅

Time

✅

Cunning

✅

Ignorance

✅

Connections

✅

Stature

✅

Less Competition

✅

The advantages of being young seems to equal the advantages of being old … at least when it comes to starting companies.

Historically young people have a way higher failure rate … but they also have a much higher rate of creating an iconic company (Google, Facebook, Microsoft, Apple, etc.).

In the past there was a tension between young and old. The young having big advantages in some societies and the old having big advantages in others. If I had to pull a number out of my butt, I would say that the best age to start a company has been 34 (not exactly “young” but definitely not old).

The best age to start a company will get much higher as computers are becoming a bigger part of our lives …

How the age advantages shift with computers: advantage to the older

Computers significantly change the advantage calculation.

Computers give younger people more access to wisdom through easy access to knowledge. The compounding advantage that older people have had in the past is going to be less important in the future. Computers also make it easier to find people and get in touch with them — so the Who-You-Knows are going to be less valuable in the future — and younger people, while still having less access to connections, are at less of a disadvantage here.

But computers help older people IMMENSELY.

Computers are the world’s best way to get access to raw brainpower. And as more brainpower tasks are getting taken over by computers, people with money (older people) will have a significant advantage over those that don’t (younger folks).

The proliferation of tech services also advantage older people. You can get access to the best APIs and services with dollars. Of course, most people (especially older people) will have trouble selecting and managing vendors. Most people (especially old people) are going to be trapped in the 20th century paradigm (one that rewards hiring and growing people). The most important business skill in the 21st century is the ability to select and manage vendors. But the older people that can successful navigate the new world will have an advantage.

As computers get stronger, it gets easier and easier to buy time and brainpower. We already have compute-on-demand (AWS) and people-on-demand (UpWork).

The biggest disadvantage that remains for older people is being trapped in an old way of thinking. If science really advances one funeral at a time, innovation could be significantly slowed as older people have more advantages (and are living longer).

One of the advantages that older people have that seems to be not going away is lack of competition. It used to be that very few 24 year olds ever thought about starting a company (especially those that had lots of opportunities). Even when I started an Internet company in college in the 1990s, it was really strange to have a student entrepreneur. Today it is becoming easier and easier to for 24 year olds to start companies — easier to get training, knowledge, and seed capital. YCombinator and other institutions have significantly promoted entrepreneurism among the young. My guess is that the number of amazing twenty-somethings starting companies has gone up at least 5 times in the last decade … and that trend is happening all over the world.

But people over 50 are still not starting companies in large numbers. It never was big, and I see no anecdotal evidence that it is growing. People that have been successful in the 30s and 40s are rarely opting to get back “in it” in their 50s. Instead, they are opting for easier and less stressful lives. So the few 50-somethings that do start companies could have increasing advantages. Especially those that still put in the long hours. (Even Bill Gates, one of the best entrepreneurs ever, hung up his business cleats before he turned 50).

More people in their 50s SHOULD start companies. It is actually a great time to start a company. Many people in their 50s are empty nesters (or at least no longer have super young kids). They can actually travel more and work harder than those in their 40s because they have fewer family obligations. They are usually more financially secure (maybe have paid off their mortgage already) and potentially more willing to take some sort of financial risk. And people in their 50s have so much more energy today than in years past — people live healthier, are more active, etc.

What are the societal implications of computers giving older people advantages?

The most obvious implication is wealth inequality. If older people get more advantages as they age, their wealth will compound faster. Coupled with living longer (and being active longer) means more wealth inequality.

Since the person in their 50s is more likely to build a one-to-N business than a zero-to-one business … it could mean less innovation for society and more incrementalism.

But it also could give hope to millions of people who are over the age of 50 and still have big dreams and ambitions. Ambition shouldn’t end at 45. Computers can keep ambition going way longer than in the past.

This also means that MORE 50-year-olds should start companies. However, I don’t think they will. So the few 50-year-olds that do should see very big advantages.

Summation: They advantage of getting older is growing. Computers are getting better at doing what young people do.

As computers get better, there are massive advantages of being older Older people (over 50) and getting more advantages from computers than younger ones. We should expect to see a huge renaissance the productivity of older business people in the future.https://t.co/SZr7HCQkMt

For the last 2000 years, one of the most important skills someone could have was the ability to plan ahead. Those that could plan ahead would reap massive awards, those that didn’t would starve in the winter.

But there has always been a tension between the forgetful creative genius (the absent-minded professor type) and the Planner. Of course, the most successful people were the combination of the Planner AND the Creative Genius (like Bill Gates and like Warren Buffett) … but that is a real rarity. For the last 2000 years, you were MUCH better off being the planner than the creative-type unless you were the BEST creative in your field. The 1,000,000th best planner still did very well.

The Planner is typically someone who is really good at seeing the likely future and making plans to address it. For instance, 2000 years ago, it was really important to plan for winter. Things did not grow in the winter so one needed to store food. In fact, thinking about food was extremely important because harvests were not certain so you would need to save grain from a good harvest to cover an eventual shortfall year.

The forgetful creative genius (the absent-minded professor) was at a big disadvantage in society because of their lack of planning skills. At the same time, the Planner (less creative but very good at logistics for the future) was needed for most tasks.

While both skills (planning and creativity) are important, the future will need more creatives types and less planners.

A history of the Planner advantage

Being a Planner 25,000 years ago (as a hunter gatherer), while important, did not pay huge dividends. You mostly wanted to avoid being eaten by lions or bitten by poisonous snakes. And you had a limit to how much you could succeed because humans where generally confined to small tribes of people.

But as the farming revolution spread and we domesticated, planning became more and more important. By the time the Renaissance and (later) Enlightenment hit, Planners could rule vast lands or get very wealthy.

Napoleon would have passed the Mashmallow Test

Napoleon Bonaparte surely would have passed the Marshmallow Test.

Then came the industrial revolution and Planners became even more in demand. Alfred Sloan, the famous CEO of General Motors, was an incredible planner.

But planning was not just important in becoming a successful business person. Planning was ESSENTIAL in every-day life.

In 1990, the people with great social lives were the planners. If you did not not plan to meet your friends, you might not be able to meet them. In the pre-mobile phone era, you needed to be constantly planing ahead. The rewards, both economic and social, went to the planners.

And yes, there were still some extremely successful forgetful creative geniuses like Einstein. But Einstein had a brain like Einstein. He was an exception.

Even the most famous 20th Century artists were Planners

People think that “creative geniuses” are not planners. But in the 20th Century (the century were planning mattered most), most of the great artists were planners.

Warhol was a planner. Picasso was a super Planner. And other “artists” are planning machines. The successful comics like Seinfeld and Chris Rock were always planning. Most of the best actors, musicians, etc. have been Planners. Planning was how you got ahead.

Until recently.

In fact, we’ve reached Peak Planner.

Today, it is easier than ever to do something in the last minute.

Want to watch a TV show? Not that long ago you’d have to plan to watch it. Seinfeld was available to watch only on Thursday at 9p. Later, when DVRs came, you’d still have to plan by setting up your DVR. Non-planners often had to resort to watching infomercials. Today, you just go watch the great show whenever you want.

Want to go on a good vacation? It is actually possible to plan the whole thing that day.

Need a ride to the airport? You can call a Lyft or Uber a minute before.

Want food? The biggest problem is picking from one of the 400 apps that help you do that.

Want to meet a special someone? Swipe right on Tinder.

Even businesses need less planning. When I stated LiveRamp in 2006 I had to plan ahead to buy servers. I remember the day when we moved our colo to a new host and we had a checklist of over 250 items. I fondly remember the celebration when we completed the move. But need more compute power for your application today? Simple to spin up more instances on Amazon Web Services.

You don’t even need to plan for office space — WeWork gives you office space on demand.

And you can even get workers on demand through UpWork and Mechanical Turk.

On-demand services are built by Planners to give non-Planners an advantage

The best planners are working themselves out of a societal advantage because they are spending their time planning logistical companies that give small benefits to other planners … but very large benefits to the absent-minded professors.

Coordination is getting easier and easier

Coordination … especially between 2–10 people … is getting easier and easier. Not that long ago, if you wanted to meet someone you’d have to spend a lot of time coordinating it. You’d break out a map and plan your route. You’d call them a few days ahead of time and meticulously plan where to meet.

Today your mobile phone takes care of all of this in real-time. No need to coordinate. It is Planning for Dummies.

The Marshmallow Test will not be as important 50 years from now

The famous Marshmallow Test predicted that people who were good at delaying gratification would be more successful. These are people who better appreciated the value of compound interest. But in a future world where planning is not as needed as today’s world, delaying gratification may not be as important.

I’m a planner and I benefitted from it.

And yes, you can still get big economic benefits if you plan. I pay half price when I buy my GoGoAir Pass on the ground instead of in-the-air. I can save a lot of money by packing a chocolate bar rather than buying one at the airport. But the benefits to planning, while significant, ain’t what they used to be.

Yeah, I plan meticulously to queue up my reading so that I always have something good to read. I save book and movie recommendations from people. But while this lack of spontaneity has generally served this Generation Xer well, it is likely not a core skill that someone born in the last decade should be focusing on.

Summation: While people that do well on the Marshmallow Test will still have an advantage … that advantage will be much smaller 50 years from now as it was 50 years ago.

Thought experiment: How would Amazon enter the venture capital business?

Use data from AWS to inform investment decisions

Amazon can leverage its proprietary data from AWS (Amazon Web Services). Amazon’s edge is that most of the best technology start-ups are built on its services. Amazon has a lot of information about how much these companies are spending, what services they use, what technologies they use, and more.

The AWS data could be extremely predictive and give Amazon early signs that companies are growing fast or reaching an inflection point. And it can use the data as a better diligence check of a company … for instance, the data could help determine which companies that claim they have “AI” are real and which are just marketing.

Amazon could significant up-end venture capital (more than even Softbank did) from their proprietary access to AWS data and their willingness to reduce fees.

Using this data to invest in public companies would likely not be legal since it could be deemed as inside information. But using it for private companies is something Amazon could do.

Of course, Amazon’s worry is that some of their AWS customers would get mad and move to Azure (which is the biggest risk of going into the VC business) … but that could be managed. Amazon could just use information from the AWS bill (and not have to see any real trade secret information) to make the initial selection of companies they might want to focus investing in. Then, of a company gives its consent, the Amazon VC team can view server logs, etc.

Which leads us to the second thing: “your margins are my opportunity”

Amazon can win VC deals the way it wins in all its other businesses: price and convenience.

On price, Amazon can offer much better terms than traditional investors that need to take high management fees and carry. Amazon wouldn’t need to do that and it would not need to, want to, or be able to (because of conflicts) take board seats. So it would have a lot more leverage … especially in the late funding stages where data is increasingly important.

And while Amazon could potentially try to buy equity, it could also instead just focus on debt (which is a product it is already familiar with — see below).

Venture capital firms’ returns net of fees (management fees and carry) have historically been very low. But if Amazon really focused on its investments, it could earn an extremely high real return.

Extreme Convenience: The easiest way to get expansion capital

Imagine logging into AWS and being presented with a term sheet. Just click here, agree to these simple terms, and we will wire $10 million to you. It takes less than 5 minutes. Yes, that seems crazy. But it IS possible.

Amazon gives its merchants loans today (and it is an extremely good business). Square also gives its merchants loans. Both Amazon and Square use its proprietary data to make loans just to businesses they are confident will pay them back. Those loans perform extremely well. Square Capital is heralded as a fantastic business. They can do this because they have unique data … and they can give an attractive price (lower interest rate) and make it more convenient (like the ability to get it in one click). There is no reason Amazon can’t give loans to AWS customers.

Amazon could create a product that gives companies funding at super attractive terms with just one click. As an added bonus to cash flows, Amazon wouldn’t even need to wire these companies the money. It could instead give companies AWS credits. If a company is spending $500k/month on AWS and believes it will continue doing so in the future (as many technology companies are), getting $10 million in AWS credits is pretty much the same thing as getting $10 million in hard dollars.

Other examples of successful technology companies starting venture capital firms

Amazon would not be the first big technology firm to start a successful venture capital firm. Both Google and Salesforce have extremely large (and, I’ve heard, very successful) VC investments (in the billions of dollars for Salesforce and in the tens of billions for Google). Apple does not have a VC firm (even though it also has a huge data advantages). But while it seems against Apple’s ethos to run a VC firm, Amazon relishes in challenging new industries and using its proprietary data to its advantage.

Debt would likely be easier to initial product than equity

The first victims of AWS funding private companies would not likely be tradition VC firms. It would more likely be the venture debt companies. That could significantly hurt some of the traditional debt providers (like Western Technology Partners) and some of the new aggressive players (like TPG, large hedge funds, and other new lenders).

Prediction: Amazon will not start a VC firm

If Amazon was a little less ambitious, it would enter the venture capital business line. The only reason Amazon doesn’t start a VC division is precisely why it could: because the VC industry is small and the gains, while in billions, may not be worth Amazon’s effort.

Also: Amazon might be worried this could hurt their AWS business. Certainly many responses to my Twitter trial balloon believe this:

Also… it’s been pitched internally a dozen times. Went nowhere.

— Matt Mireles | Accelerate or Die 📈 (@mattmireles) January 23, 2019

Summation: while Amazon will not likely challenge the incumbent venture capitalists and venture lenders, it is a really interesting thought experiment to see how it could.

The car companies (like Toyota, GM, Ford, Honda, BMW, etc.) have a tough business.

First: it is SUPER competitive. It is one of the most competitive businesses around. No one car company is even close to dominant. The competitive nature means it is very hard to make money (and even harder, though not impossible, to really invest for the future).

Second: auxiliary revenue streams are going away. For a while, car companies were able to sell a suite of additional services like OnStar (subsidiary of General Motors), SiriusXM, navigation, financing, and more. Fewer of these services are value-add today (than just 5 years ago). The smart phone has taken over these services and is generally 10x better.

Third: Car companies are not capturing good data. Presumably car companies could capture maps of cities (from the cameras), traffic, breaking, driving habits, tire pressure, and more. Presumably they could use the data to give the drivers better experiences. They could even have additional revenue streams selling the data (like TV manufacturers do). But very few car companies take advantage of this data. It is not clear WHY they don’t collect it. Collecting the data is easy. Sending the data to a central system is easy. This is not hard stuff.

Yes, Tesla does this. But Tesla does a lot of things incredibly well. It is unfathomable why ALL the car companies do not collect this data. And they are not ceding their position to Tesla. It is not Tesla they should be worried about. They are ceding their position to the smart phone OS (like Apple and Google) and to some of the great apps on the smart phone. And while the driving data collected on the smart-phone is massively inferior to what could be collected by the car, it is much better than tiny data. And tiny data is what most car companies are collecting today. It makes no sense, but a lot of things in business make no sense.

Fourth: Car ownership is declining due to the abundance of new transportation options. Uber and Lyft are amazing. So are the new scooters. And electronic bikes are becoming bigger for the suburbs. Forget self-driving cars (that may not be a reality for 50+ years). Declining car ownership is happening now. It is like cord cutting … it starts off very slowly but then picks up steam rapidly.

Summation: the car companies are in a tough spot. Some great ones will innovate but many are going to be in more and more trouble in the years to come.

(thank you to Evangelos Simoudis for helping me think through this topic)