Every month I try to share the most mind-expanding links to read/watch/listen. If you find these interesting, please do share with your friends.

Here are five links worth reading…

Beliefs are Fashions by Erik Torenberg People don’t choose beliefs based on logical value or merits, but based on how much status they can garner in their tribes.

Little Ways the World Works by Morgan Housel If you find something that’s true in more than one field, it’s probably important. A look at the rules from statistics, philosophy & evolutionary biology and the broader truths we can learn from them.

Listen: David Epstein: Never Underestimate the Generalist In a complex world, thinking broadly is more important than ever yet society increasingly values narrow subject expertise. Explore the pitfalls of specialization and how to think about your own career.

Geographic mobility is one secret of successful immigration by Tyler Cowen Without hometown roots, immigrant families are more likely to move to areas with higher opportunity, resulting in better outcomes than their native-born economic peers.

Correlations go to One, in Good Ways and Bad by Byrne Hobart Markets, both in the economic sense and the financial one, are machines for producing valuable information about how the probabilities of different events are connected. There is no free lunch.

Bonus (Listen): Gary Marcus: The Failed Promise of Artificial Intelligence Is AGI really right around the corner? What will it take for AI to reach the next threshold of capability? Gary Marcus offers some insight and a critical perspective in a complex field.

Graph of the Month: Quality of AV systems don’t scale with wealth

Books:

The Making of the Atom Bomb by Richard Rhodes (Must Read) (this is a really long book but one of the best books i have read in the last 20 years) HT: Matt Clifford

Every month I try to share the most mind-expanding links to read/watch/listen. If you find these interesting, please do share with your friends.

Here are five links worth reading…

The Current Thing Why is everyone up in arms about something new every month? Due to mimetic desire, social psychology, and social media, the mainstream converges to an intellectual monoculture.

Listen: Liv Boeree: Developing a Probabilistic Mindset Probability seeps into every aspect of our lives, yet most people don’t apply it all to their daily activities. Liv lays out frameworks everyone should apply to life, society and science.

The Purpose of Technology Technology’s proximate purpose is to provide leverage and do more with less – effectively reducing scarcity. But its long-term purpose is to reduce mortality, the main source of scarcity.

Optimism It’s a lot easier to sound smart as a cynic than as an optimist. But the upside of optimism is unlimited, it’s like a call option on society. So why do so many people choose to be pessimistic?

Trying Too Hard Being a novice can be more valuable than being an expert. Everyone wants to be an expert, whether it’s law, medicine or investing. But often, the best answer is the simple, obvious one.

Bonus (Advice): 103 Bits of Advice I Wish I had Known Life advice from one of the greatest optimists. An invaluable list covering abstract and tactical topics that would certainly make everyone a better person.

Bonus (Listen): Antonio Garcia Martinez: A New Approach to Regulation Regulation which appears great on paper often has many unintended consequences. This is especially true when it comes to big tech and privacy regulation.

Graph of the Month: Trust your gut, but only sometimes

Books:

Range by David Epstein HT: David Epstein, Brett Sylvia

Every month I try to share the most mind-expanding links to read/watch/listen. If you find these interesting, please do share with your friends.

Here are five links worth reading…

The New Science of Alt Intelligence The perceived objective of AI has always been to mimic human behavior. But most researchers today don’t want this. Instead, they’re focused on building what’s called “alt intelligence”.

Listen: Glenn Fogel: The Greatest Acquirer in History M&A is messy and most of it fails. Fogel has somehow managed to complete several successful acquisitions while building Booking Holdings. What does he know that others don’t?

Why don’t nations buy more territories from each other? You can count all the transactions involving the sale of land from one country to another in the past century on one hand. Why don’t more countries sell off land? Tyler Cowen explores why.

Listen: Barry Nalebuff: A Radical New Way to Negotiate Most negotiations are unfavorable for all parties because more time is spent bargaining for a larger slice of the pie and not enough time is spent defining the pie. Defining the pie can unlock win-win scenarios in most negotiations.

Bonus (Listen): Introduction to Mimetic Theory Most people want what others have. Rene Girard coined the term Mimesis, the desire to imitate one another, and concluded that it was Mimesis that drove most of society’s problems.

Graph of the Month: Slack is great… until it’s not

Companies and orgs can promote and thrive from tension

All companies have tension.

There are at least two axes where tension resides:

Long-term vs Short-term projects.

Doing things right vs doing things fast.

This tension exists within a company, between departments, within a department, and even between cofounders. This tension is very healthy and often propels companies to succeed greater than they would without the tension.

All companies have tension. Two axes: Long-term vs Short-term projects. Doing things right vs doing things fast. pic.twitter.com/mEdSW6aXbY

This is the classic tension that many companies, especially start-ups, think about. Every individual has a personality trait that has them fall somewhere along the axis.

Mark Zuckerberg’s famous line “move fast and break things” was Facebook’s motto for its first ten years (2004-2014). Moving fast and putting out new features is why Facebook was so successful. But in 2014, Facebook decided to move on the axis from “doing things fast” to “doing things right” and Zuckerberg changed the motto to the less-catchy “Move Fast With Stable Infra.” That change is representative of the tension that exists within companies … and also the evolvement of all companies.

Most venture-backed start-ups err on doing things fast verses doing things right. Moving fast is the main advantage of a small organization because all large organizations move rather slowly. So one of the best vectors to compete against more entrenched incumbents is speed.

In my piece “Pace, Tempo, Speed, and OODA loops” I lead off with the quote from Jeff Bezos: “Being wrong might hurt you a bit, but being slow will kill you.”

The best strategy for larger organizations is to pick a small number of really important things to do — and make sure those things are done right. A great example of “do things right” strategy is Apple … but even Apple also needs to care about speed.

Even within companies, there is a LOT of tension between doings things fast and doing things right. If you were 100% on one side or the other, the company would almost surely fail.

Cofounders themselves can have conflict. I’ve seen successful start-ups with two cofounders where one has a “fast” personality and the other has a “right” personality. I’ve seen successful start-ups where both cofounders have “fast” personalities. Curiously — I have never seen a successful start-up where both founders have a “right” personality — those have always failed. In the end, speed wins for start-ups.

There are hundreds of amazing companies that sell software and tools to data scientists and machine learning teams. In fact, many of the best companies in the last 15 years have been exactly that.

But outside of SafeGraph (where I work), there are almost no companies that specialize in selling data to data scientists.

Why?

Partially it is because it is MUCH easier to get to $10 million ARR by selling applications (traditional SaaS). Partially it is just tradition coupled with stagnation. Partially it is because venture capital firms have been wary of funding data companies. And, most convincingly, being a data-only business is less exciting to most entrepreneurs because data is a supporting role (see the last section on data and humility).

But selling data to data scientists is starting to be a big business.

Selling data (DaaS or Data-as-a-Service) historically has not been a great business. Outside of Zoominfo and a few others, there have been almost no pure-play data unicorns built in the last 20 years.

That’s because very few companies had the ability to make use of raw data in the past. 10 years ago, only the most advanced engineering teams were able to make use of external data. But that’s changing. An order of magnitude more companies buy data today than did five years ago. That’s because a good engineer with a tool like Snowflake can be as productive as a great engineer was 5-10 years ago.

This is happening across industries.

One example is hedge funds. Not that long ago, just ten funds were buying significant alternative data. Today it is still under 100. But there are 500-700 funds that are currently making the investment to ingest large amounts of data.

The number of hedge funds that buy significant alternative data is still really tiny … but growing pic.twitter.com/cAmVMVXj6b

The #1 rated session was an interview with Todd McKinnon, CEO Okta — it was excellent and I highly recommend it.

My presentation was the #2 rated session. Here is the full video:

And here is the full learnings:

(1) Avoid good opportunities

the MOST IMPORTANT advice I can give you is to avoid good opportunities.

avoid good opportunities like you work to avoid the coronavirus.

Good opportunities must be avoided at ALL costs.

this is true if you want to build a great company … but this is JUST AS true in life.

the more successful you become, the more good opportunities are going to come at you. soon you will be swimming in good opportunities.

again, that’s true for companies and true for you individually.

let’s first dive into this advice individually and then show it applies to building a business.

let’s say you are 22 years old and don’t have any money. well then you are likely going to see very few opportunities to invest and most of them will be bad. but as you gain wealth, you will see more opportunities to invest — and many of them will be good. but even the good opportunities take time and effort to review — so it is in your best interest to do everything possible to wait only for the great opportunities.

this is even more true when running a company. the possibilities of the number of things you can do to grow your business are endless. you can launch new products, be better at recruiting, speak at SaaStr, and so much more. my advice, have some sort of rubric that allows you to ID good opportunities and avoid them.

but how do I know when an opportunity is just good and not great?

my simple heuristic: if the opportunity has few obvious downsides, it is almost certainly NOT a great opportunity. all great opportunities have very big and very obvious downsides.

of course, just because it has obvious downsides doesn’t mean it is a great opportunities — it still is more likely to be a bad or good opportunity … but if you see something with no obvious downsides, it almost certainly is not great.

this is also true with people you hire. if you want to hire a 10xer, that person will almost certainly have glaring faults. anyone that you can hire without glaring faults will, at best, be good — they will certainly not be great.

summary: avoid good opportunities like you avoid COVID-19

(2) Delegate things you are good at

most people advise us to delegate things you are not good at. they advise to surround yourself with people that have different strengths and different weaknesses.

this is the conventional advice.

maybe someone on your board already gave you this advice.

most of us have heard this advice many times over the years.

but this is terrible advice. don’t listen to it. ignore it. take it outside in the backyard and bury it. stab it and kill it.

do the opposite.

instead: Delegate the things that you are good at.

I know this sounds really strange … so let me explain.

the things that are the EASIEST to delegate are the things you are already good at. you know how do those things really well. you might already be an expert in them. you can break down these things well. you can also hire for these things.

so delegating these functions will, for sure, have the highest success rate.

if you are a great engineer, who do you think you will be better at hiring — other great engineers or great salespeople?

the answer is obvious — you will likely hire super engineers and very mediocre salespeople.

so the first thing you should always delegate are the things you are best at.

I cannot stress this enough.

you even see it in all great companies – they rarely get great in things that are not traits of their founders.

for instance, Marc Benioff is the world’s best software marketers. he was an amazing software marketer ever before he started Salesforce. he’s incredible. he’s hired great marketers and delegated to them. Salesforce continues to be great at marketing.

but Marc Benioff is not a great UI/UX person. while he’s been able to acquire great UI/UX people through acquisitions over the years (Stuart Butterfield, CEO of Slack, is one of the world’s greatest), the Salesforce product still suffers from having one of the worst UI experiences.

and guess what? it hasn’t mattered.

it is better that Benioff focused on his strengths.

you should focus on your strengths too — you cannot be all things to all people. focus on being great at just a few things.

let’s look at the napkin graph (above).

on the y-axis is things you are good and things you are bad at. the x-axis is things you love to do and things you really hate doing.

when you get a chance, try to fill out these quadrants for yourself.

the easy thing is to delegate as much as possible on the things you are already good at.

build systems to make delegation easier. hire super talented people and work on up-leveling them.

now you have two other buckets left.

for the things you like to do but are not yet good at … work on investing in yourself. get a coach. read. learn. try a few different things (and know that you will fail). while it is unlikely you will ever become great at these things … you can get yourself to good. once you are good, you can better effectively delegate (and hire).

now there are things that you are bad at and you also do not like doing. my advice in this quadrant is to do everything possible to get leverage through APIs or software … or maybe you do not need to do them at all. remember, you don’t have to do everything to have a super company. there can be many functions that you either outsource or just not do.

the great thing is that the number of vendors you can choose from is growing exponentially. you have amazing choices.

the number one skill to have in the next 20 years is the ability to select and manage vendors — almost every company now has more vendors than employees.

(3) Do the opposite of “smart” people

take a look at what the smart people around you are doing … and do the opposite.

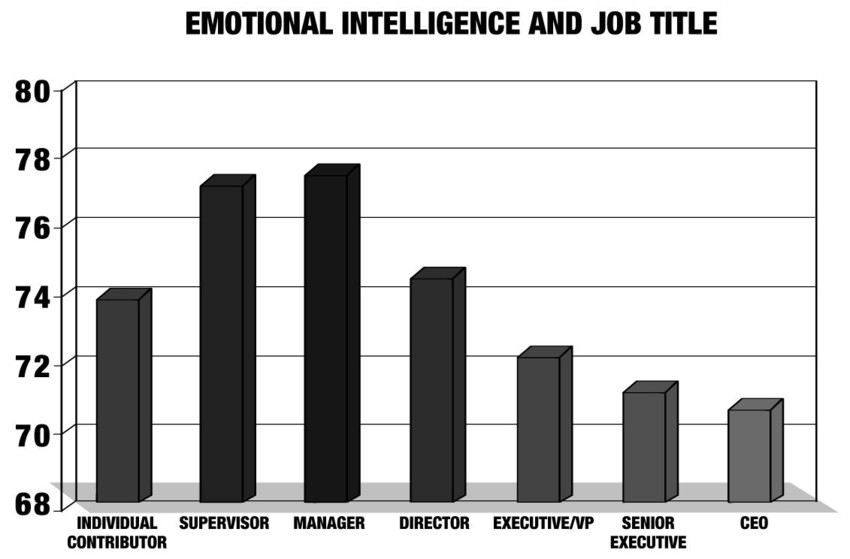

Most great CEOs have high EQ (Emotional Quotient) and Emotional Intelligence (also known as interpersonal intelligence). While EQ’s importance is not as high as it once was, it still is extremely important, especially for leaders.

So what to do if you are a low-EQ CEO?

Most successful leaders that don’t have high EQ tend to have off-the-charts IQ. But what if you are a low-EQ leader whose SAT score was under 1590?

This post is a self-help manual for those low-EQ leaders.

The first half of this piece offers some ideas to improve your leadership skills as a low-EQ leader. The second half provides insight into what it’s like to be a low-EQ person and how low-EQ correlates with other common character traits. This piece should be valuable both for low-EQ leaders (I wish I read this myself ten years ago) and anyone that works closely with low-EQ leaders.

But that sugar-coats it — having a low-EQ is a severe disadvantage as a leader. It is a real blind spot.

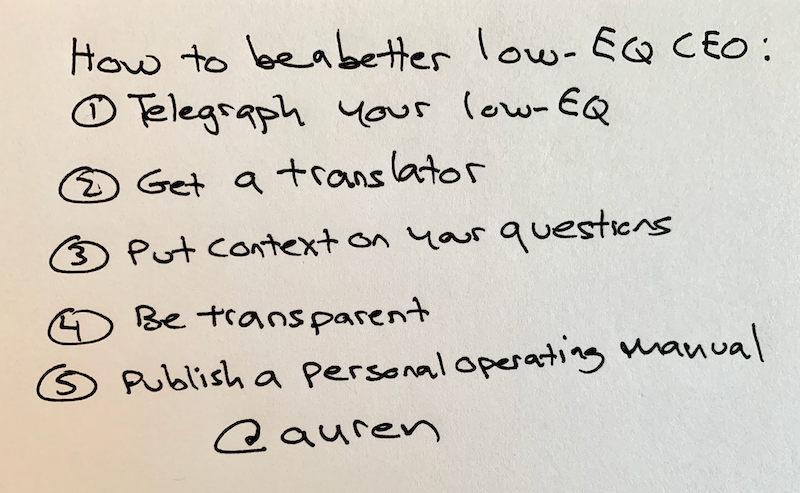

How to be a better low-EQ CEO.

There are five core things low-EQ leaders can do to help their relationships:

Telegraph your low-EQ abilities to others. ☎️

Rely on other high-EQ colleagues to be a translator.

Be explicit about the context of your questions. 🙋

Be honest and transparent.

Create a personal operating manual. 📕

Warning: this piece will be a lot more personal than most of the other things I write (personal sections in italics — feel free to skip … of course, high-EQ people tend to enjoy more personal stories 🙂 ).

1. Telegraph your low-EQ abilities to others ☎️

If you are low-EQ, everyone you work closely with must know … because most of these people will come into any relationship with the expectation that you are adept at reading non-verbal cues. If they know you cannot read their faces (reading faces is highly correlated with EQ), they will work with you to compensate in other ways.

It is also important to remind people that they will be less likely to read your face. So they should not be assuming things from your nonverbal cues … because you are less likely telegraph your feelings consistently. Yes, we all have tells. But a grimace from a low-EQ person could actually mean that they are happy … so others should not read into these cues too deeply.

One leader I admire mentioned:

While telling people that you are low-EQ is a good step, it’s not really fair to put the responsibility of dealing with your low EQ on them. Most people will not be comfortable being overly explicit and so you will need to draw it out of them by proactively ask questions (e.g., “how do you feel about what I’ve just said?”) and even make some assumptions (e.g., “I may be wrong (remember, I can’t read faces) but you look frustrated/happy/perplexed. Do I read this properly?”)

2. Rely on other high-EQ colleagues to be a translator.

If you were having a business meeting with someone that did not speak your language, you’d bring along a translator. A good translator not only helps translate your words but also helps you observe and adhere to cultural differences, different norms, etc.

Low-EQ leaders need to rely on translators in the office too. They can entrust other executives with translation and interpretation. So, find 1-3 people that can help you translate what others are thinking and explicitly enlist their help. They can tell you when someone does X, they really mean Y.

I’ve recently done this at SafeGraph — a few of the people on our leadership team have extremely high EQs, and they have helped me understand more complex situations. Without their insights, I would have misread many situations.

Of course, it is really important that these translators are trustworthy and do not use the situation to interpret things in their favor. You want to find high-EQ people that also think clearly about the best long-term interest of the organization.

3. Be explicit about the context of your questions 🙋

When leaders (even those who have high-EQs) ask questions to others in their organization, their questions can often be interpreted as directives (even if they are just innocent inquiries).

One way you can guard against this is to be explicit about what kind of question you are asking. I learned this from Brian Gentile. I’ve been experimenting with five hash-tags that I now add to questions I ask (which could be live or in written form):

Telling

Selling

Consulting

Brainstorming

Learning

The #Telling hashtag is when you want to be explicit that this is a directive coming from you. This is very rare, but occasionally, it is important to be explicit about that.

The #Selling hashtag is when you are selling an idea to other people in your organization. You think this is the right way to go, and you are working on getting their buy-in. Of course, you are open to changing your mind, but you are coming into the conversation with a strong opinion about what to do.

The #Consulting hashtag is when you want to dive into a recommendation someone else has made and understand it better. You’re in coach-mode. You might be able to offer your advice on how to improve it even more. Or by understanding it better, you might be able to help another part of the organization.

The #Brainstorming hashtag is when you just want to brainstorm an idea. You are coming in with few preconceptions and want another person or a group of people to help get to a good answer.

Lastly, the #Learning hashtag is just to help you satisfy your curiosity. I often use #Learning when asking our VP Engineering about a specific technology decision or machine learning technique. In this case, I’m curious and just want to learn.

Since I started doing this, I have found that 90% of my hashtags are either Consulting, Brainstorming, or Learning. I’m rarely Telling or Selling. But, in the past, without being explicit about my inquiry, people at my company have misinterpreted my questions as being directives instead.

These hashtags are a very analytical response to being low-EQ. But being analytical is often something that low-EQ leaders are good at … so use it to your advantage.

4. Practice honesty and transparency.

Low-EQ leaders need to telegraph their thinking to others more than high-EQ leaders. This is because people are much more likely to think a low-EQ person is not telling the truth (even though there is no relationship between honesty and EQ).

One of the best ways to do that is to be honest and transparent.

I personally used to keep things close and never telegraph high-level strategy to the company. Today, I am much more open with everyone in the organization about how we should think things through … and am also much more open when I don’t know something or have changed my mind (which is often). I send out an email to the team at least twice a month diving into a strategic topic and giving the team a lens into how I am thinking about it.

You can compensate for your low-EQ by clearly explaining your thinking to others. This takes out the “guessing game” for your co-workers. Because people are more likely to misunderstand low-EQ people, you will need to go to greater lengths to show your thinking. It’s like seventh-grade math where your teacher made you show your work (and not just the answer). You have to show your thinking and where it comes from.

Of course, high-EQ people should practice honesty and transparency too. They just don’t have to work as hard to do it. Low-EQ leaders need to put in the extra effort to actually build systems around honesty and transparency.

One CEO I admire told me:

Another technique I’ve been using to great effect: tell people how I’m feeling. I realized that I’m not good at telegraphing my positive emotions — especially over Zoom. I’ve been making a conscious effort to say things like “I’m very happy with this”, “I’m proud of what you did”, “this makes me very excited”, etc. At first it sounds cheesy to say, but it’s been so helpful. Especially in terms of building up credibility for when I have to share a negative emotion like, “I’m disappointed with how this turned out.”

These systems become even more important in a large company. High-EQ leaders might find it harder to transition from a 100 person company (when you can know everyone) to a 1,000 person company. Their high EQ might have allowed them to get by (at 100 employees) without formal systems to translate their understanding and empathy. This is especially true in a world where everyone was in the same office (low-EQ leaders are at less of a disadvantage in remote-first companies).

5. Create and share a personal operating manual 📕

When I first started working with my friend Jeff Lu, he suggested we write a personal operating manual and send it to each other. I had never heard of this concept before but I now send mine to everyone that reports to me or I meet regularly with.

An operating manual defines how people should work with you. It should clearly define your personality quirks so that others can get the most out of you. For example, here is a quote from mine:

Opportunities over threats

Auren is wired to seek out opportunities and discount threats. He is generally focused on what can yield the 20x return and can discount the 1x loss. Auren can be dismissive of problems because he has high confidence they can be solved.

An operating manual is good for everyone to write and share with their colleagues. But it is especially important for low-EQ people. One thing I do in my operating manual is specifically call out my low-EQ:

Direct over indirect

Auren only understands points that are directly made. Auren rarely picks up on indirect points (like non-verbal cues). Auren has mild prosopagnosia — which means he is poor at recognizing faces. (Facial recognition has a high correlation with EQ.)

Another good thing to do in an operating manual is to share your results from personality tests that you think are relevant — for instance, Enneagram, Myers Briggs, and StrengthsFinder tests.

If you had a recent 360 review, it might be useful to provide a link to the review from the operating manual, so your colleagues can dive into more details to help them understand how to get the most out of working with you.

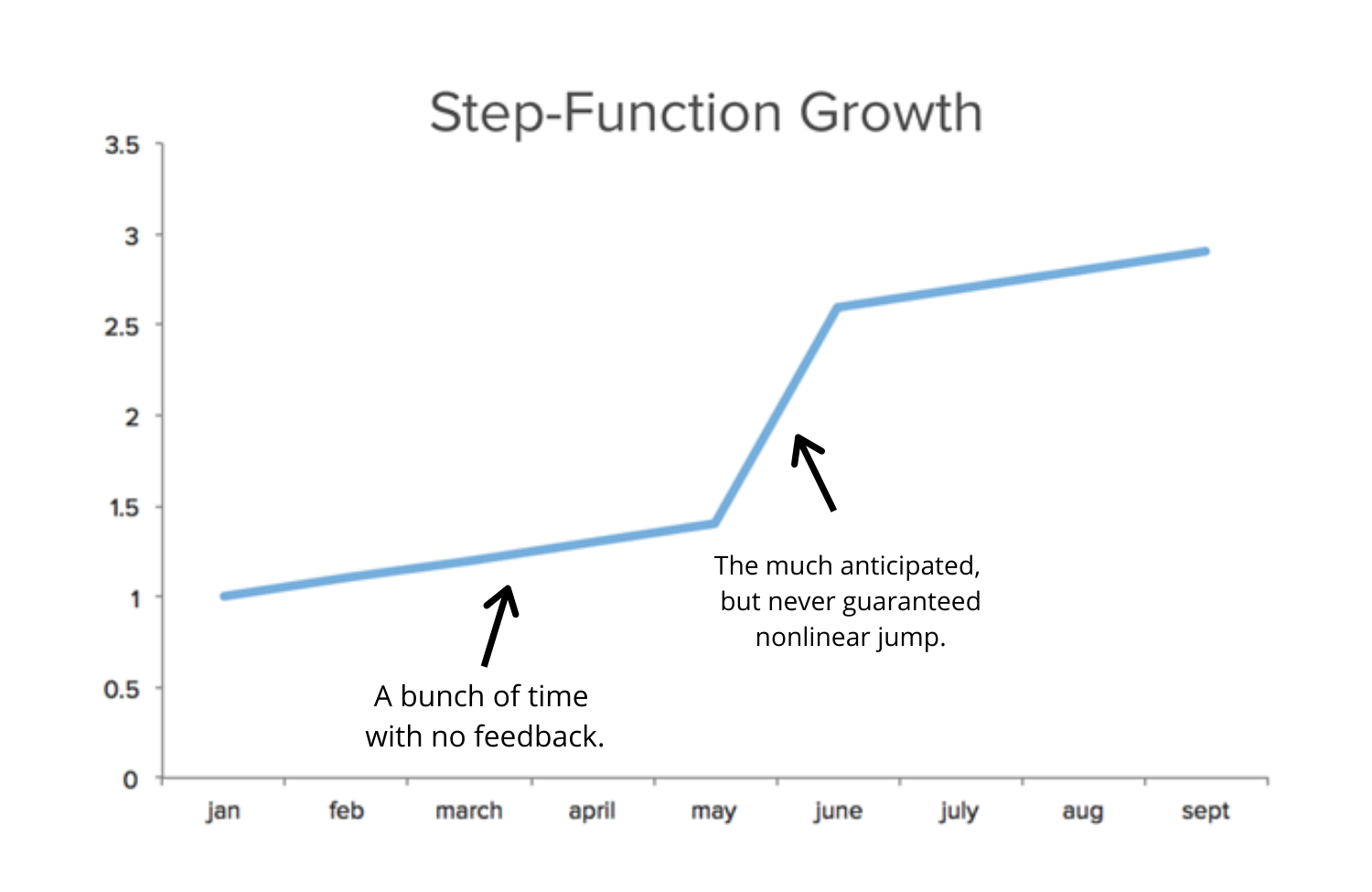

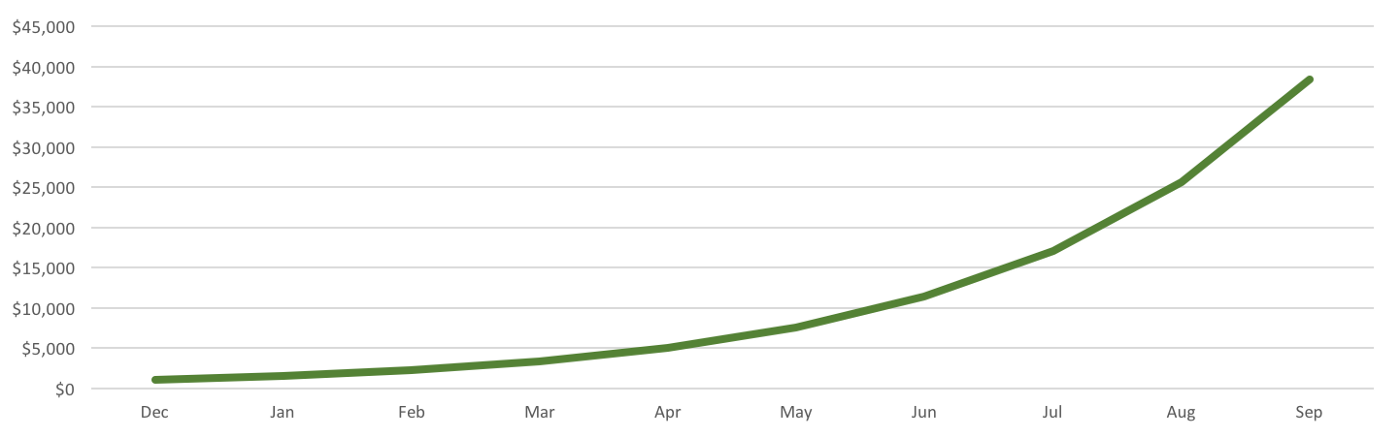

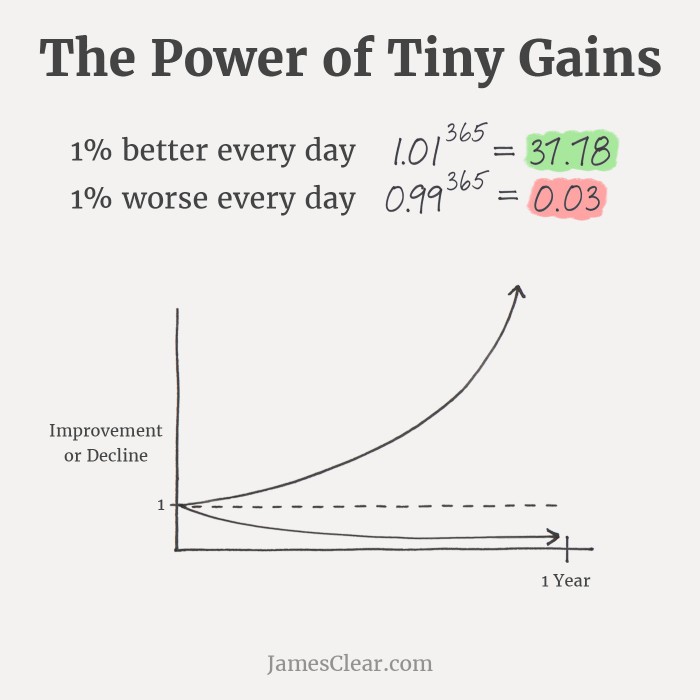

Business building happens by a series of 1% improvement. But business domination comes with step functions. You can build a very good business with just the first one. But you need both if you want to build a great business.

One-percent improvements can build a solid company.

You can build a good company with slow, constant progress. By building through a series of 1% improvements, a start-up can grow to $8M ARR in year 3, $16M ARR in year 4, $26M ARR in year 5, and $40M ARR in year 6, etc.

Here’s what that growth looks like:

The nice thing about continually making 1% improvements is that they have a high likelihood of success and a high likelihood of helping the business. One can follow a playbook from other similar companies about what to do and how to up-level and make investments. And no company can be successful without consistently making 1% improvements.

One-percent improvements add up over a long time.

Seventy-two 1% improvements results in a doubling of the output of the company. The faster you make these 1% improvements (OODA loops), the quicker you get to the doubling. It works, and it can work well over the long term.

If your company could get just 1% better every day for an entire year, you’ll end up 37X better after 365 days. Writer James Clear has a great chart for this:

SafeGraph has six core Values and one (“Judgment is the x-factor”) of them was basically lifted almost verbatim from the LiveRamp Values because it is the most important value to me:

Judgment is the x-factor. It is essential that every team member at SafeGraph makes key decisions autonomously, so that we move fast and limit bureaucracy. But as Voltaire (sometimes attributed to Spider-Man’s Uncle) said, “with great power comes great responsibility.” To make great and effective decisions at all levels of the company, we need to (1) clearly communicate the company’s strategy to all team members; (2) hire super smart teammates that work hard; (3) only hire people who have demonstrated sound judgment and are deserving of our trust.

It is really powerful to work at a company that exclusively employs people with good judgment. It allows you to move faster. It builds trust amongst coworkers. It eliminates bureaucracy.

To do that one has to actively discriminate against people with bad judgment: which means you need to make this one of the core criteria during interviews (and through observations once someone starts).

The main reason that you want everyone in the company to have good judgment is so you can have fewer “rules” which allows you to move faster. Much faster. The more rules, the slower you will move. The more you trust employees to make decisions, the more decisions will get made.

“At SafeGraph, I try to deliberately make as few decisions as possible. I deem it a failure if I need to make a decision … because that means we are moving slower in that area. That does not mean I don’t make any decisions — I do. But those are failures I hope to improve upon in the future. Additionally, you don’t want the management team making decisions.”

Of course, when you trust others to make decisions, it means they won’t always be made exactly the way you want them to be made. You need to be ok with that. That is a by-product of decentralized decision-making.

As a CEO, you can still reserve the most important one-way door decisions for you to make … that way if you completely screw up the company at least you can only blame yourself 🙂 In fact, that is one of the reasons I love being a CEO — I have only myself to blame. For instance, you’ll likely be extremely involved in hiring people (even if you ultimately empower the hiring manager) because having people with good judgment that your team can trust to run with the ball is so important.

While most of SafeGraph’s values are aspirational (and we can fail at them), judgment is an absolute must. If we hired someone without judgment, we would have to terminate them … as people with bad judgment are a real cancer on organizations. Because people with bad judgment create rules.

When we sold LiveRamp to Acxiom in 2014, the first thing I did was read the Acxiom HR handbook. There were lots and lots of rules. One rule I found particularly interesting was “you cannot do cocaine on premises.” After talking with the SVP of HR, I found that yes, there was a story of someone actually caught doing cocaine in the Acxiom bathroom. Rather than just immediately firing the offender, they also thought it was necessary to add a rule. But you cannot enumerate all rules (there was no written rule against heroin or meth … there was no written rule stating people must wear clothes to work). One must eventually rely on people for their judgment.

Good judgment is the answer to lots of rules. And lots of rules make decisions take longer which means the company would inevitably move at a slower pace (see recent scribe on pace). Judgment is fused with pace. All things being equal, a company filled with people with good judgment can outrun a company that is not.

Of course, judgment does not mean you need to stop and contemplate all your moves. It should be ingrained in what you do. It does not mean you never make mistakes. It does not mean you never have a bad day or act in a way you regret. But it does mean you don’t need a seminar to know that harassing someone is a bad thing. It means you don’t need a training to know you don’t discriminate on race. Good judgment knows that one must act in the best long-term interest of the company.

clearly communicate the company’s strategy to all team members

It is really hard to act in the best long-term interest of the company if everyone is not in sync about the company’s long-term interests. That is why it is really important to clearly and frequently discuss the company’s strategy. The more you are all in sync about where the company is going in the long-term, the more you can rely on judgment of your fellow teammates to get you there. Planning becomes less important with judgment because everyone knows where the company is headed.

One of the primary missions of the CEO is to help everyone in the organization understand the long-term strategy. It is actually really hard to do that and I have frequently failed at it at SafeGraph, LiveRamp, and other organizations I have been a part of.

I recently wrote about why hiring is harder in a recession than it is during an economic expansion. But, just because it’s hard (it is always hard) doesn’t mean you shouldn’t try. You should always be looking for A-Players to bring onto your team.

Hiring obvious A-Players is really hard because everyone else knows they are obvious and they will be extremely sought over (and very expensive). That doesn’t change in a recession.

So, if you want to find the A-Players that are available, you can’t look for the obvious ones. You have to find the diamonds in the rough who don’t look like precious stones.

To find A-Players in a downturn, look for people that other people in Silicon Valley would discriminate against.

You want to find people that were passed over by other tech companies for reasons other than their talent and give them a chance.

You can start with women and minorities. They are still very much discriminated against. Of course, few people in Silicon Valley will outwardly state that they want to discriminate against women and minorities. And many companies even have active programs to reach out to them. You might not have an advantage in landing female and minority A-Players because there are a lot of other companies competing for this talent pool.

In addition to women and under-represented minorities, there are a lot of other categories of people who are actively discriminated against in Silicon Valley including:

Boomer generation (people born 1946-1964)

People that went to third-tier universities

Religious people (even slightly religious people)

People who are politically conservative

People with thick accents

People who are overweight

People who smoke cigarettes

People who are socially awkward

Let’s take a closer look at each of these categories.

Hire people over 55.

Tech companies tend to be extremely biased against people with grey hair. This is especially true of older people who are seen as “past their prime” or recently part of a company that crashed and burned. It is extremely rare for a tech company to hire an individual contributor that is over 45. And this trend is likely more pronounced during an economic downturn.

There are plenty of people who, in 2008, ended up taking the Director-level job at Digg instead of at Facebook (even though they had job offers at both). The ones who went to Digg are seen as past their prime and the ones that went to Facebook are living on their own private island and serving on the boards of directors of hot start-ups. Just because the person made a wrong financial choice 12 years ago does not mean they cannot add immensely to your company.

Bezos believes that you should be able to feed your team with just two pizzas

“Crazy thought experiment: Imagine a new type of company that decided to only do what it was really good at and essentially outsourced everything else.”

Because revenues of private companies tend to be secret, most venture-backed companies have historically bragged about how many employees they have. A CEO will say: “we went from 100 to 200 employees last year” as if fast employee growth is always a good thing.

But this is changing: there is a new status game brewing between companies concerning who has the fewest number of employees, centered around who is engineering greater amounts output with less staff. Indeed, the freedom to iterate quickly is status. More resources along with lower headcount means that they can dominate new markets. This is because they are tripling down on their strengths.

In the future, those who achieve the greatest results with the least number of employees will be admired above all others; the key statistic to look at is the go-forward net revenues per employee because it best encompasses the company’s leverage. What matters is each employee’s productivity and how the business itself can scale?

revenue per employee is an important metric to understand over time.

companies with flat revenue/employees over years (which is the case in many tech companies) often mean that the company is not run very well and does not have a ton of leverage.

This statistic doesn’t just ring true for the technology space, rather any business should be aiming to maximize that metric. By doing so, every employee feels and acts like Warren Buffet; they’re investing their capital (time and skill) into the company. Every good CEO should be spending time trying to increase their employees’ productivity, which is the strongest form of leverage the company retains.